3

A Long-Memory Model for Multiple Cycles with an Application to the US Stock Market

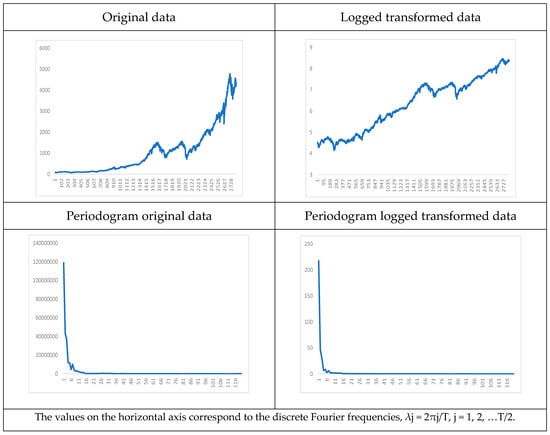

www.mdpi.comThis paper proposes a long-memory model that includes multiple cycles in addition to the long-run component. Specifically, instead of a single pole or singularity in the spectrum, it allows for multiple poles and, thus, different cycles with different degrees of persistence. It also incorporates non-linear deterministic structures in the form of Chebyshev polynomials in time. Simulations are carried out to analyze the finite sample properties of the proposed test, which is shown to perform well in the case of a relatively large sample with at least 1000 observations. The model is then applied to weekly data on the S&P 500 from 1 January 1970 to 26 October 2023 as an illustration. The estimation results based on the first differenced logged values (i.e., the returns) point to the existence of three cyclical structures in the series, with lengths of approximately one month, one year, and four years, respectively, and to orders of integration in the range (0, 0.20), which implies stationary long memory in all cases.

You must log in or register to comment.